Partnership Income Tax Malaysia

The most common tax reference types are SG OG D and C. The cost of an asset that you can depreciate is reduced by the amount of any GST credit that you are entitled to.

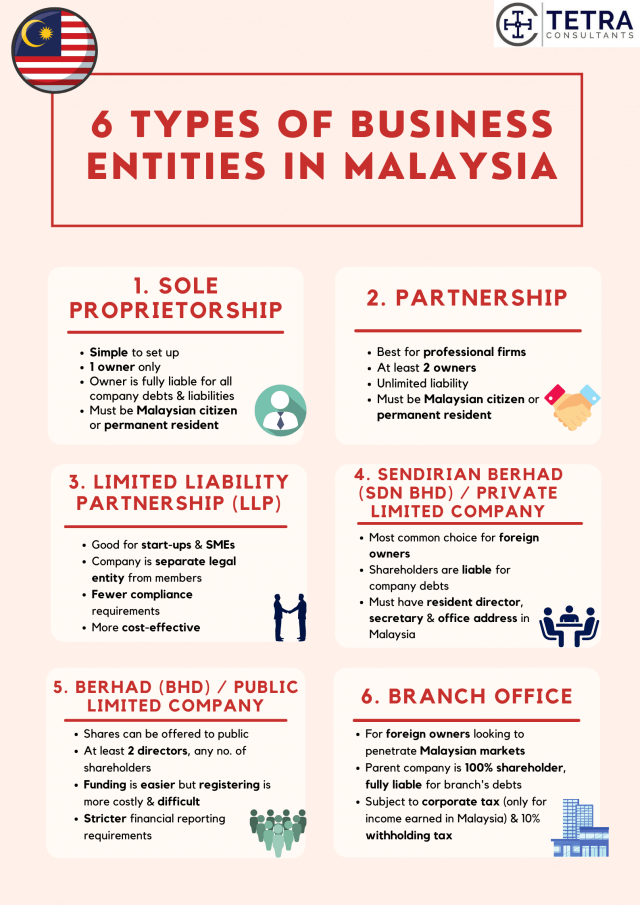

6 Types Of Business Entities In Malaysia Tetra Consultants

The Inland Revenue Board of Malaysia Malay.

. SG 12345678901 Tax Reference. Thus for a Nevada resident selling interests in a partnership ie an intangible asset. Space Income Tax Number Maximum 11 numeric characters SG 10234567090 or OG 25845632021 Non-Individual File Number Type of File Number 2 alphabets characters.

There are different types of tax incentives offered in Malaysia in the form of tax exemptions allowances related to capital expenditure and enhanced tax deductions. Paragraph 4f of the Income Tax Act 1967. Section 2 of the Income Tax Act 1967.

Using the correct HMRC reference number. Case Report Appeal to the High Court from decision of the Special Commissioners of Income Tax. In the case of allowances there is a provision to carry forward the unutilized allowances until it is.

Takaful business 60 AB. A generally applicable principle of state income tax law is that income from the sale of intangible assets is attributed to the resident state of an individual realizing the income unless the asset has in some way acquired a business situs or connection with another state. The income is deemed as a business sources if maintenance services or support services are comprehensively and actively provided in relation to the real property.

It helps HMRC identify which employer they are dealing with. You might also use other HMRC services such as VAT or Corporation Tax receiving separate reference numbers for each of these tooKeep a list of relevant reference. TF or C etc space Income Tax Number Maximum 10 numeric characters TF 1023456709 or C.

Although the income is exempted from tax tax will have to be paid on the dividends paid on tax exempted income. To put it simply. For capital assets such as machinery you may be entitled to an income tax deduction for the assets decline in value depreciation.

During any current tax season or calendar year a timely tax return would be prepared and e-filed for the previous calendar year. Provisions applicable where partnership is a partner in another partnership 58. That is when working out the decline in value use the cost of the asset less any GST credits youre entitled to.

Any individual earning more than RM34000 per annum or roughly RM283333 per month after EPF deductions has to register a tax file. With effect from Wef 1 January 2022 income derived from outside Malaysia and received in Malaysia by tax residents will be subject to tax. A special allocation of partnership income to the retiring partner if the payments are Section 736a payments because they were made to either 1 a.

Income attributable to a Labuan business activity of a Labuan entity including the branch or subsidiary of a Malaysian bank in Labuan is subject to tax under the Labuan Business Activity Tax Act 1990 LBATA. Form BE refers to income assessed under Section 4 b 4 f of the Income Tax Act 1967 ITA 1967 and be completed by individual residents who have income other than business. Malaysia Information on Tax Identification Numbers Updated 2 December 2020.

Lembaga Hasil Dalam Negeri Malaysia classifies each tax number by tax type. The SME company means company incorporated in Malaysia with a paid up capital of. Chargeable income of life fund subject to tax 60 B.

Keysight Technologies Malaysia Sdn Bhd V. A tax season prepare and e-file returns for the previous calendar or tax year is from January 1 until October 15 of any current year. Chargeable income reduced rate and exempt dividend 60 AA.

Director General of Inland Revenue V. During January 1 2022 - April 18 2022 you prepare and e-file taxes for the tax year of. Malaysia adopts a territorial scope of taxation where a tax-resident is taxed on income derived from Malaysia and foreign-sourced income remitted to Malaysia.

Insurance business 60 A. For small and medium enterprise SME the first RM600000 Chargeable Income will be tax at 17 and the Chargeable Income above RM600000 will be tax at 24. Income receivable by partnership otherwise than from partnership business 59.

In Malaysia income derived from letting of real properties is taxable under paragraph 4a business income or 4d Rental income of the Income Tax Act 1967. Each employer who registers for Pay as You Earn with HMRC has a unique tax reference number. Your Income Tax Number consists of a tax reference type of 1 or 2-letter code followed by a 10 or 11-digit tax reference number.

Director General of Inland Revenue. However foreign-sourced income of all Malaysian tax residents except for the following subject to conditions to be announced which is received in Malaysia is no longer be exempted with.

Business Income Tax Malaysia Deadlines For 2021

2

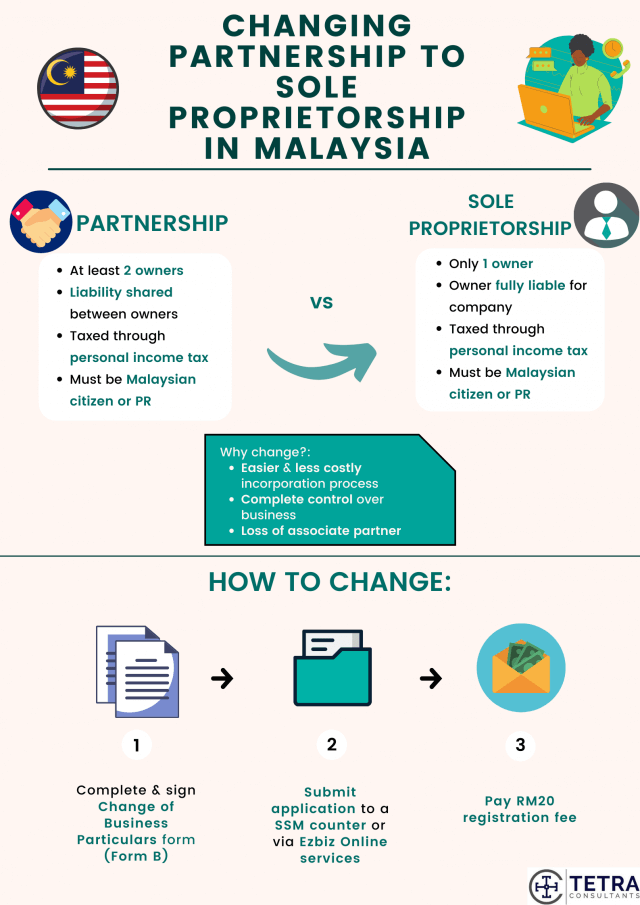

Steps To Change Partnership To Sole Proprietorship Company In Malaysia Tetra Consultants

Deadline For Malaysia Income Tax Submission In 2022 For 2021 Calendar Year L Co

No comments for "Partnership Income Tax Malaysia"

Post a Comment